Trump intensifies trade war with threat of 30% tariffs on EU, Mexico

President Donald Trump on Saturday threatened to impose a 30% tariff on imports from Mexico and the European Union starting on August 1, after weeks of negotiations with the major U.S. trading partners failed to reach a comprehensive trade deal.

In an escalation of a trade war that has angered U.S. allies and rattled investors, Trump announced the latest tariffs in separate letters to European Commission President Ursula von der Leyen and Mexican President Claudia Sheinbaum that were posted on his Truth Social media site on Saturday.

The EU and Mexico, both among the largest U.S. trading partners responded by calling the tariffs unfair and disruptive while pledging to continue to negotiate with the U.S. for a broader trade deal before the deadline.

Mexican President Claudia Sheinbaum said she was sure an agreement can be reached. “I’ve always said that in these cases, what you have to do is keep a cool head to face any problem,” Sheinbaum said at an event in the Mexican state of Sonora.

“We’re also clear on what we can work with the United States government on, and we’re clear on what we can’t. And there’s something that’s never negotiable: the sovereignty of our country,” she said.

A bar chart showing the value of EU imports and exports from/to the US, along with the balance of trade in 2023.

Trump sent similar letters to 23 other trading partners this week, including Canada, Japan and Brazil, setting blanket tariff rates ranging from 20% up to 50%, as well as a 50% tariff on copper.

The U.S. president said the 30% rate was “separate from all sectoral tariffs,” indicating 50% levies on steel and aluminum imports and a 25% tariff on auto imports would remain.

The August 1 deadline gives the targeted countries time to negotiate agreements that could lower the threatened tariffs. Some investors and economists have also noted Trump’s pattern of backing off his tariff threats.

The spate of letters showed Trump has returned to the aggressive trade posture that he took in April when he announced a slew of reciprocal tariffs against trading partners that sent markets tumbling before the White House delayed implementation.

‘UNFAIR TREATMENT’

But with the stock market recently hitting record highs and the U.S. economy still resilient, Trump is showing no signs of slowing down his trade war.

He promised to use the 90-day delay in April to strike dozens of new trade deals, but has only secured framework agreements with Britain, China and Vietnam.

The EU has hoped to reach a comprehensive trade agreement with the U.S. for the 27-country bloc.

Trump’s letter to the EU included a demand that Europe drop its own tariffs. “The European Union will allow complete, open Market Access to the United States, with no Tariff being charged to us, in an attempt to reduce the large Trade Deficit,” he wrote.

Von der Leyen said the 30% tariffs “would disrupt essential transatlantic supply chains, to the detriment of businesses, consumers and patients on both sides of the Atlantic.”

Trucks cross into the United States via the Zaragoza-Ysleta border bridge, after U.S. President Donald Trump announced imposing a 30% tariff on imported goods from the European Union and Mexico, starting August 1, 2025, in Ciudad Juarez, Mexico, July 12, 2025. REUTERS/Jose Luis Gonzalez Purchase Licensing Rights

She also said while the EU will continue to work towards a trade agreement, it “will take all necessary steps to safeguard EU interests, including the adoption of proportionate countermeasures if required.”

A bar chart showing the top exported goods from the European Union to the United States in 2024.

Mexico’s economy ministry said Saturday it was informed the U.S. would send a letter during a meeting on Friday with U.S. officials.

“We mentioned at the roundtable that it was unfair treatment and that we did not agree,” the ministry’s statement said.

RATE FOR MEXICO LOWER THAN CANADA

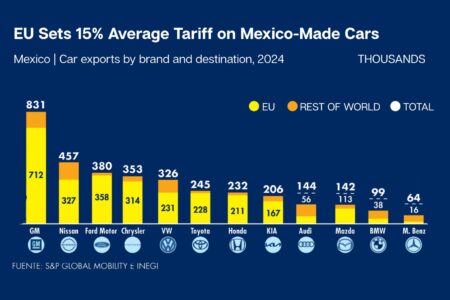

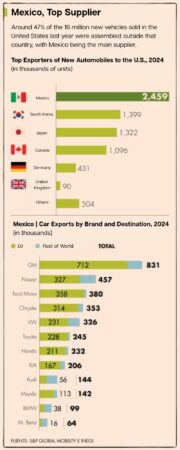

Mexico’s proposed tariff level is lower than Canada’s 35%, with both letters citing fentanyl flows even though government data shows the amount of the drug seized at the Mexican border is significantly higher than the Canadian border.

“Mexico has been helping me secure the border, BUT, what Mexico has done, is not enough. Mexico still has not stopped the Cartels who are trying to turn all of North America into a Narco-Trafficking Playground,” Trump wrote.

China is the main source of the chemicals used to make the opioid fentanyl. According to U.S. authorities, only 0.2% of all fentanyl seized in the U.S. comes from across the Canadian border, while the vast majority originates from the U.S.-Mexico border.

Mexico sends more than 80% of its total exported goods to the U.S. and free trade with its northern neighbor drove Mexico to become the top U.S. trading partner in 2023.

The EU had initially hoped to strike a comprehensive trade agreement but more recently had scaled back its ambitions and shifted toward securing a broader framework deal similar to the one Britain brokered that leaves details to be negotiated.

The bloc is under conflicting pressures as powerhouse Germany urged a quick deal to safeguard its industry, while other EU members, such as France, have said EU negotiators should not cave into a one-sided deal on U.S. terms.

Bernd Lange, the head of the European Parliament’s trade committee, said Brussels should enact countermeasures as soon as Monday. “This is a slap in the face for the negotiations. This is no way to deal with a key trading partner,” Lange told Reuters.

Jacob Funk Kirkegaard, a senior fellow at the Brussels-based think tank Bruegel, said Trump’s letter raised the risk of retaliatory moves by the EU similar to the flare-up between the U.S. and China that rattled financial markets.

The chart show European Union(EU) trade balance over the years with countries outside EU as well as with United states.Trade surplus with U.S. reached € 197 billion in 2024.

“U.S. and Chinese tariffs went up together and they came back down again. Not all the way down, but still down together,” he said.

Trump’s cascade of tariff orders since returning to the White House has begun generating tens of billions of dollars a month in new revenue for the U.S. government. U.S. customs duties revenue topped $100 billion in the federal fiscal year through to June, according to U.S. Treasury data on Friday.

The tariffs have also strained diplomatic relationships with some of the closest U.S. partners.

Japanese Prime Minister Shigeru Ishiba said last week that Japan needed to lessen its dependence on the U.S. The fight over tariffs has also prompted Canada and some European allies to reexamine their security dependence on Washington, with some looking to purchase non-U.S. weapons systems.

Source: Reuters